AGA

GAFRB

Q1:

According to GASB, the costs of which of the following activities associated with internally generated computer software should be capitalized?

○

A

selecting between alternatives for the software project○

B

converting extra data not needed to make the software work○

C

testing the software for functionality and ease of use○

D

training employees to use the softwareAccording to GASB Statement No. 51 -- Accounting and Financial Reporting for Intangible Assets, costs associated with internally generated computer software can be capitalized only during the ''application development stage.'' Activities in this stage that are capitalizable include:

Coding

Software configuration

Testing (for functionality)

Non-capitalizable activities include:

Preliminary project planning (e.g., selecting between alternatives)

Data conversion not necessary for the software to operate

Training employees

Therefore, testing the software for functionality is an activity that should be capitalized.

Relevant Reference:

GASB Statement No. 51

GFOA Best Practices -- Capitalization of Intangible Assets

Answer : C. testing the software for functionality and ease of use

AGA

GAFRB

Q2:

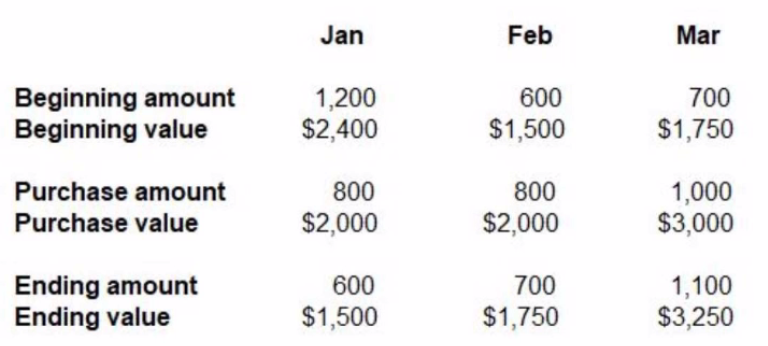

The quarterly inventory record below has been provided for use in preparing the organization's financial statements. Based upon the information provided, what method of inventory valuation is used by the organization?

○

A

FIFO○

B

average cost○

C

LIFO○

D

net weight scaleThe organization's inventory records show that the beginning and ending amounts and values change each month, and the relationship between units and dollar values suggests that the cost per unit is averaged, not fixed (as with FIFO or LIFO). Let's evaluate January:

Beginning: 1,200 units / $2,400 $2.00 per unit

Purchased: 800 units / $2,000 $2.50 per unit

Ending: 600 units / $1,500 $2.50 per unit

The ending value of $1,500 for 600 units gives a per-unit cost of $2.50, matching the purchase cost in January. This suggests the system uses a weighted average cost method rather than tracking the specific cost layers (as FIFO or LIFO would).

Relevant Reference:

FASAB SFFAS No. 3 -- Accounting for Inventory and Related Property

GAAP and GASB guidelines on inventory valuation

GFOA Best Practices -- Inventory and Supply Chain Management

Answer : B. average cost

AGA

GAFRB

Q3:

Interest accrued on the public debt is reported as

○

A

a receipt.○

B

an outlay.○

C

a cost of goods sold.○

D

a tax expenditure.Interest accrued on the public debt (e.g., Treasury securities) is considered a government expenditure. In federal financial reporting and budgeting, this is classified as an outlay, representing a payment made to meet an obligation.

It is not a receipt (revenues collected), a cost of goods sold (used in commercial accounting), or a tax expenditure (which refers to revenue foregone due to deductions, credits, etc.).

Relevant Reference:

OMB Circular A-11 -- Budgetary Definitions

Treasury Financial Manual (TFM) -- Federal Outlay Reporting

GAO Glossary -- Public Debt Interest Treatment

Answer : B. an outlay

AGA

GAFRB

Q4:

For state and local governments, a fund that is legally restricted to the use of earnings with the principal protected is

○

A

an enterprise fund.○

B

a permanent fund.○

C

an internal service fund.○

D

a general fund.

AGA

GAFRB

Q5:

Which of the following government-wide financial statements are required for state and local governments?

○

A

balance sheet and operating statement○

B

statement of net position and statement of changes in net position○

C

statement of net position and statement of activities○

D

statement of net position, statement of activities, and statement of cash flows